Has the time arrived for US carbon capture?

A combination of higher subsidies and a recognition that renewables can’t do all the work of decarbonisation looks promising for the US. Proximo and Leidos assemble a panel of experts to look at what still needs to be done.

Supported by:

Carbon capture, utilisation and storage (CCUS) is one of the most credible solutions to the hardest to abate carbon dioxide emissions. Much of the technology involved in CCUS is proven, and commercial applications are available. The 2022 Inflation Reduction Act turbocharged the tax credits available to carbon capture projects, and the US Department of Energy’s Loan Programs Office has long been enthusiastic about the technology. A wide variety of project developers and counterparties are looking at the technology closely.

Sign up to receive our Weekly Newsletter for the latest project infrastructure finance updates, exclusive insights and benefits tailored for our subscribers.

Developers are looking closely at optimising project structures - including fitting CCUS to greenfield conventional power plants and retrofitting it to existing facilities. And it is likely that the technology will appeal both to integrated utilities and independent power producers. Regulatory and financing priorities are likely to be key determinants of which business models are most suitable to deploying CCUS viably.

The final part of the puzzle is building a base of support among commercial bank lenders. Among the challenges are understanding market risk, technology risk, interface risk, the US regulatory environment, and how CCUS fits in with lenders’ sustainability mandates. Understanding how these risks can be priced and allocated will be key to carbon capture assets becoming mainstream project financings.

But the market has yet to see a limited-recourse financing for carbon capture at any real scale. Proximo and Leidos assembled a group of developers and lenders familiar with the technology to review the progress to date and look at what still needs to be done in CCUS.

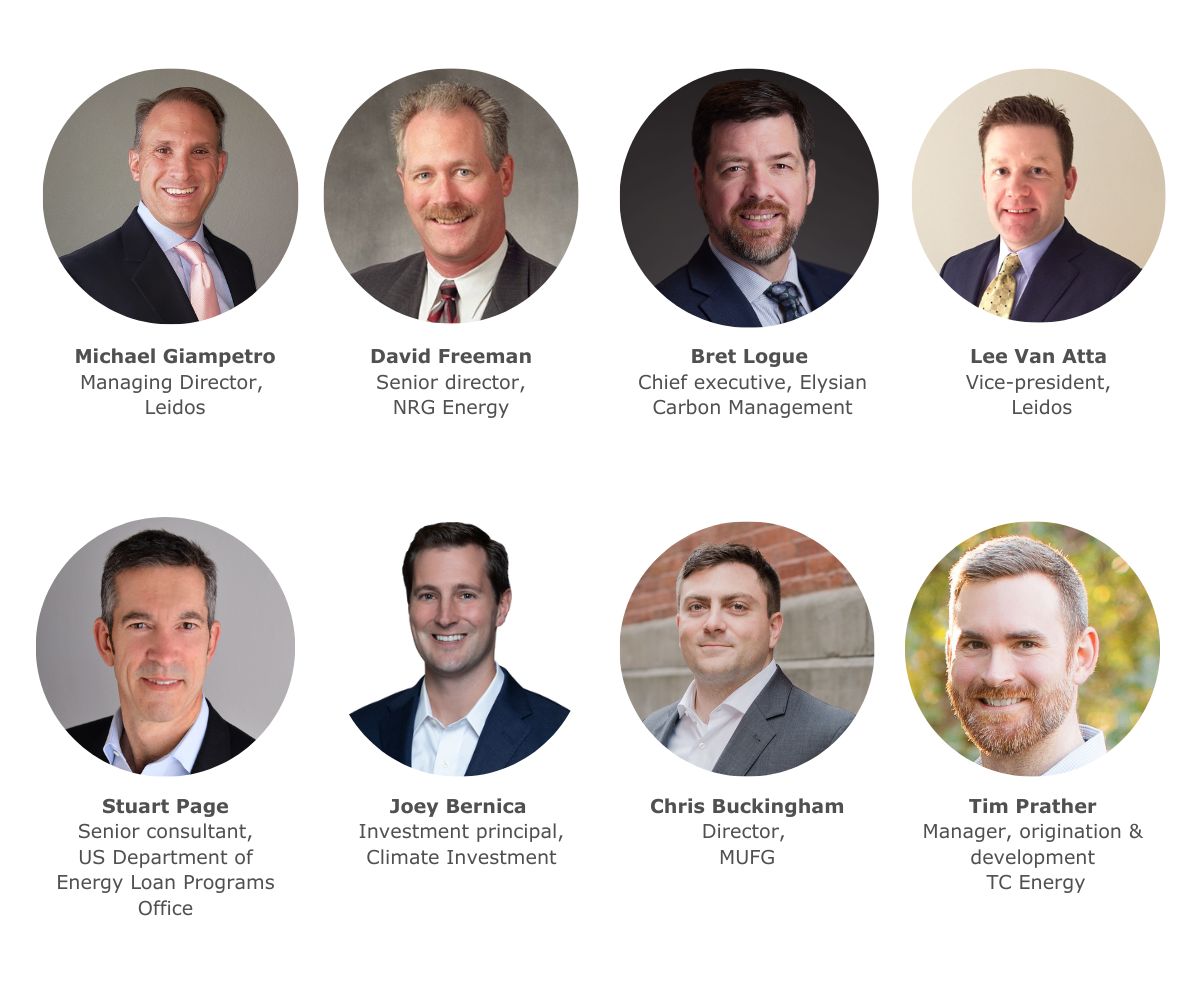

Roundtable participants:

Proximo: What’s been the general attitude of commercial banks towards CCUS so far?

Chris Buckingham, MUFG (CB): For banks that are active in the project and infrastructure finance space there's excitement, not just around renewables, but also other project finance opportunities that are contributing to decarbonisation and the energy transition. The attitude is one of cautious interest, and we certainly think that activity is picking up when it comes to CCUS, and that banks are actively chasing opportunities.

Bret Logue, Elysian Carbon Management (BL): We probably collectively have talked with 60 or so banks over the last five years. There’s strong interest in the commercial bank market, but they’re still cautious and trying to get familiar with the technology and get their credit committees ready to review large projects. We’ve also seen the shift in focus towards sustainability and the prioritisation of particular aspects of the energy transaction in line with sustainability goals. Another feature of conversations has been potential support from the government, and the interplay between the Department of Energy’s Loan Programs Office and commercial lenders.

Stuart Page, DoE LPO (SP): An applicant comes to us generally because they can’t access the bank market. Projects are not necessarily first of a kind, but they're nth of a kind where n is a small number. For a bank to perform the necessary diligence to be confident of their loan dynamics is a big ask. The role of the LPO is to get involved with these companies that are helping to catalyse change in a significant way, but really are stuck with equity as their primary capital source, and to give them leverage that is sufficient that they pass investment return hurdle rates that will make an investment happen. Whether or not these will get built is a big question of capital availability, return expectation, performance, technology, and so on. The DoE has a number of different grant facilities, including CarbonSAFE, which could help delineate subsurface geology for sequestration, build business plans and produce FEED studies.

Michael Giampetro, Leidos (MG): Most of the technologies that we've seen proposed for CCUS are proven, they’ve just not necessarily been utilised in the power sector. As a result, there is no precedent for non-recourse project financing CCUS in the power section. The lack of precedent is not a fatal flaw, the technology is proven, but is likely to result in higher levels of scrutiny until the financing structure is normalised. Further prior to the IRA, 45Q was not sufficient to incentivise power produces to incorporate CCUS into greenfield development or retrofits.

Proximo: Where does CCUS fit in with sustainability mandates?

Joey Bernica, Climate Investment (JB): Most energy and heavy industrial corporates today are thinking through decarbonisation pathways across their portfolio. Some of those pathways may involve CCUS, but there are other pathways, including electrification and upcycling, that may not. All the pathways are capital intensive, and some corporates might be overwhelmed by the options, so when they encounter capital-intensive projects, they tend to delay the decision in the hope that the decarbonisation pathway becomes clearer in a few years. That said, some corporates have identified blue hydrogen and post-combustion carbon capture as the best way to decarbonise their assets and are committed to CCUS. They are investing in technologies through their corporate venture capital groups, and carrying out feasibility and FEED work on their projects. I believe this is likely to lead to a number of projects being built further down the road, but we're not seeing shovels in the ground today.

Tim Prather, TC Energy (TP): Companies who you wouldn't think would prioritise something like CCUS always want to bring it up in conversations. From technology companies to the traditional large industrials and power utilities to even coffee and beverage producers. Many of these companies have a need to decarbonise a specific Scope 1 emissions from their facilities that correspond to a large portion of their overall corporate CO2 emissions. The market sees value in the tangible nature of emissions being intercepted, filtered, and injected underground for permanent sequestration on the order of thousands of years. This is a direct and measurable way to decarbonise compared to paying, say, for a forestry offset. I can show you a meter at the capture portion of your plant that says, I'm capturing X quantity of cubic feet of CO2 from your flue gas stream and then here's my injection wellhead, showing you the same amounts being permanently stored. I think as project economics start to creep into the black, we'll see more widespread adoption.

BL: There's a growing recognition that post-combustion capture or point source capture is a more permanent solution compared to nature-based solutions. But it’s a multi-year process that takes a long time in terms of investigation, development and permitting, in the form of the Class VI permitting process with the Environmental Protection Agency. As more substantial locations emerge for long-term permanent storage that will help accelerate the development of the large point source capture facilities. There has been a lot of initial interest in direct air capture, as potentially the cleanest possible option. But until we address point source emissions it's maybe a bit early for an exclusive focus on direct air capture. Rather than pulling water out of the tub while the tap is still running at full blast, it's probably worth controlling the tap first.

TP: We shouldn't neglect greenfield hydrogen and ammonia industry development, or new power generation facilities, that are incorporating CCUS concepts early in the engineering phase as an option. Companies do not need to make a decision about a facility that exists today, that is already emitting and part of their Scope 1 emissions reduction plan. It’s more about future-proofing new development - partly by extending the timeline to incorporate these designs and partly because it's easier to plan and engineer a new facility that incorporates carbon capture equipment than retrofit in some instances. Many existing facilities don't have physical space onsite. Additionally, CCS is very geology dependent. For large emitting facilities along the Texas, Louisiana, or Mississippi Gulf Coast, or in other areas like North Dakota and Wyoming, it's achievable, but in an area like the Appalachian Basin it's just not as cut and dry.

David Freeman, NRG Energy (DF): At NRG our focus is squarely on serving our retail customers, which vary from the very small to commercial. We have experience of bringing carbon capture to reality from Petra Nova in 2017. To quote Winston Churchill, “don’t let perfection be the enemy of progress.” A focus on perfect zero carbon, entire life cycle, every minute of the day, solutions are not sustainable from an economic perspective. It is critical to keep power economically viable for end users, and within that we are technologically agnostic. We focus on competitive retail power, and are not a monopoly that can pass on the costs and risks of a decision for 20 or 30 years to captive customer bases. Our customers fix their relationship with us on a yearly basis, and will switch to an alternative if it is more viable a year from now. We will have to roll up our sleeves doing the hard work to select smart energy technologies in advance of making capital commitments.

SP: We’re seeing some interesting and novel technologies such as sustainable aviation fuels, and if you can create an economic product out of the carbon that you're capturing, that's obviously a better outcome than depending on a 12-year tax credit for your economics. We find that in general, CCUS for natural gas processing, ethanol, and hydrogen are economic at $85 a ton sequestered. But combined cycle natural gas-fired power generation is not yet in the money given where technology is – about $95 to $120 for capture, and that's excluding transportation and sequestration. But there's a learning curve as you execute on these projects and start deploying more at scale. We are dependent on companies that can add voluntary additional cost coverage in sequestration. That's really why we're trying to help fund some of these projects by providing low-cost debt.

Proximo: Does the bank market see any difference between adding carbon capture equipment to existing generating capacity and building a new plant that is carbon neutral. Would banks, looking at emissions from their existing portfolios, be more keen to invest in abating existing emissions?

CB: There will be different groups of enthusiastic parties to look at deals depending on what the application is. But we want to be careful to avoid focusing our discussion only on banks, because the US has very dynamic and active capital markets, which we often access for clients financing single assets. Some of the CCUS projects are going to be sizeable from a capex perspective, and we have spent time talking to rating agencies and institutional investors to come to a view that, with sensible risk allocation there will be capital markets access for CCUS projects and businesses. We think that each institution has a different ESG personality, and a web of mandates and parameters driving decision making continues to become more complex. As you break down the components of a CCUS project and look at the use cases for decarbonisation equipment, there are some sensitivities about different aspects of it and there are potential applications where there may be limitations on appetite. Fundamentally, when the commercial model and risk allocation are digestible, these projects will be financeable. A few short years ago, there was no project finance market for financing data centres or, certain types of fibre infrastructure, or battery storage. When structures emerge that can be underwritten by commercially motivated creditors, the market will respond.

Proximo: How has the IRA bedded down for the CCUS industry?

BL: The IRA has been hugely transformational for the industry, and the Bipartisan Infrastructure Law allocated a significant amount of funding for CCUS. And so this legislation has been a substantial focus for CCUS teams for the last three years, and we should ultimately see more announcements of projects in advanced development. But despite the IRA we have seen some big increases in costs to construct these facilities. That $85 per ton number was established through very detailed discussions in 2019, but that dynamic has changed because of Covid and subsequent supply chain challenges, and is probably higher now. The previous level of the 45Q tax credit works for technologies that were fine at $50 per ton, including capture at natural gas processing or ethanol plants where you are close to storage and do not have to build a 2,000-mile pipeline. The increase in 45Q in the IRA was designed to support the technology to be used on natural gas combined-cycle plants and process-related emissions from hydrogen, cement and steel production. The IRA has been a tremendous vehicle for project development – and we just saw another $6 billion of DoE funding for the decarbonisation of industrial emissions, but we will need to see something done to address the gap caused by these cost escalations post-Covid. Still, there are additional avenues for commercial participation in decarbonisation, by getting private partners to pay a premium for a decarbonised electron or molecule. Until recently we thought there was going to be increased demand for power from electrification of vehicles and other sectors, but nothing as fast and immediate as what we are now seeing from data centres that need to cope with artificial intelligence applications. That may be an opportunity, given that many technology companies are customer facing and may be willing to pay a premium for a decarbonised product.

Lee Van Atta, Leidos (LVA): You really need carrots and sticks. The IRA provides the carrots, and the Biden administration has been attempting to put some sticks out there, but that's been more challenging. The IRA has definitely accelerated development – we’re looking at 20GW of solar getting built year after year, at least 10GW of annual onshore wind additions, plus around 30GW of offshore wind with a large amount of battery energy storage to help integrate all of those renewables. But even with that 700GW of new renewables, our models still leave us with a fairly carbon intensive US power grid, with some coal and a pretty substantial amount of natural gas. The solution to enable a fully decarbonised US power grid will need to come either on the fuel side or through CCUS. We had expected that there was a fairly long runway to allow CCUS or other solutions such as green hydrogen to develop but load growth is clearly back with estimates that data centres could account for another 60GW of demand, and together with load growth from the electrification of the transport and building sectors could push demand growth from around 1% to 2% per year. With that level of load growth, we could be looking at a reliability crisis, and this has created an opportunity for retrofits of existing coal-fired power plants with CCUS and new build natural gas-fired CCGTs with CCUS. While capacity markets should reflect the increasing reliability needs, and power market prices should go up, some of these assets will need long-term contracts. Even if you have a 12-year 45Q credit on a 30- to 40-year asset, someone will need to support that after the credits are done.

BL: Part of the reason why a combined cycle plant is not supported by an $85 price is that we’re applying a 12-year model to a much longer-term asset. A contract does not need to go all the way out to 25 years, but some kind of stick to encourage private purchasers to emerge would be a huge help.

Proximo: Are there likely to be any issues with the implementation of the 45Q credits?

BL: The 45Q regulations are relatively straightforward, and while how transferability and the timing of direct pay are not perfect, they are nowhere near as challenging as the tax credit regime for hydrogen. In fact, we have heard that a number of blue hydrogen projects that had expected to take advantage of 45V might switch to the 45Q regime because it’s easier to implement. But it is of less value than if a project can achieve 4-5 kg of CO2 per kg of hydrogen.

JB: 45Q provides a very clear signal at $85 a tonne fixed, compared to Canada or the EU, where carbon is publicly traded, but it’s volatile and difficult to hedge long-term. $85 is not enough for most post-combustion carbon capture projects, and there will need to be other economic incentives - or disincentives. Apart from 45Q credit levels, there are a multitude of non-economic impediments preventing projects from being built. These include permitting, both for pipelines and sequestration. Then there's uncertainty around costs and a reluctance on the part of EPCs to give wraps on these projects, and complex multi-party contracting between the Capture Co, the Transport Co and the Sequestration Co. Plus, there's lack of availability of debt financing, and also there's subsurface uncertainty. So, you need to account for all the additional risks that I just mentioned on top of the economic price signals that 45Q sets.

SP: The IRA took 45Q from $50 to $85, and lowered the threshold of materiality for emissions and created transferability. The transfer market is becoming more liquid, though developers may only see 90% of the value of transferred credits. For DAC [direct air capture], the credit is actually $180, but corporate responsibility voluntary payments are allowing DAC plants to get built. Several data centres are being announced with 24-7-365 availability of clean energy, and only geothermal, hydro, nuclear and carbon capture can meet that requirement. The cost of power in AI business plans is small relative to the revenues, so a small voluntary carbon capture payment might be feasible.

BL: Carbon capture looks expensive until you're trying to buy Nvidia chips.

Proximo: What risks have not got enough attention so far?

MG: If it's an existing thermal asset, performing a life extension study of the asset is critical. We expect the utilisation of proven CCS suppliers will be required, though there are plenty of big players. Getting a permitted well is non-trivial. Utilising a proven and qualified EPC is important, whether you are doing greenfield or retrofitting. A final consideration I would mention is how the addition of carbon capture equipment is going to challenge the dispatch and operational considerations for a power generation asset? It may not be as simple as following load and serving traditional electricity markets.

Proximo: Is the decision to alter dispatch profiles technical or about economics?

MG: It is probably both. CSS is not going to be able to ramp as quickly as a modern combined-cycle facility, but how sensitive dispatch will be to CCUS is still to be determined.

LVA: If the project is connected to ERCOT or PJM and not to a data centre behind the meter, there will be significant economic pressure during periods of high renewable output on dispatch. A modern combined-cycle plant is great at ramping up, say when solar comes off late in the day when prices are high and reliability is a concern, but that type of ramping operation might not work for a chemical plant that needs the CO2. This gets even more challenging as renewable penetration increases and the load profile changes due to electrification. In some markets, you're looking at a complete switch from summer peaking to winter peaking or dual peaks which drives a need for more flexible dispatchable generation resources. But we're going to be losing so much existing baseload generation that there's going to be a role for CSS to play even though there is a tremendous challenge around managing the dispatch profile in highly dynamic power markets.

DF: We're seeing solar grow very fast, and we have a good base of wind generation. Given the need for flexible generation, the need may be less for combined cycle than for peaking technologies, and R&D in battery technologies that can fill that gap for the three or four days of a severe weather event. Neither the summer peak nor the winter peak are concerns, so much as later in the day after the sun sets. In California they call it the Duck Curve, but in Texas we call it the Armadillo Curve, as people arrive home from work and the sun has set customers still need power. While we have experience with CCUS from Petra Nova, the economics are challenging not only for a new or existing combined cycle, but also for a new peaker. Pre-combustion capture, perhaps from blue hydrogen, looks more economically palatable to provide that flexibility.

Proximo: What is your feeling about the viability of carbon capture on a merchant power risk profile?

SP: We are project finance and fundamentally we're looking to mitigate the risks that we can. Purely merchant will stretch the capability of most banking facilities.

CB: Merchant is obviously more challenging. It becomes a second order risk that people need to evaluate on top of CCUS. It might not be impossible, but I wouldn't structure a non-recourse financing for a multi-billion dollar project with material merchant exposure, at least until sector knowledge in the market matures.

LVA: Most project financings that have been called merchant have had some kind of financial hedge or other revenue support. But merchant dispatch could push up operations & maintenance costs, and energy margins could be pressured by running during hours with very low market prices. Current merchant markets don't do a good job about creating a premium for carbon-free electrons, and RECs do not really work for carbon capture. We may need a separate PPA-type structure to support carbon capture since merchant markets were not designed to value carbon reduction.

DF: Our experience is a project that would otherwise be called merchant would usually have a long-term bankable tolling agreement with a buyer of power at levels that would recover a capital investment. The revenues would come from a combination of government incentives, government support for payments from carbon-intensive industries like aviation, and highly-rated offtakers such as E&P companies and/or data centres.

Proximo: What business models – and what balance sheets – are best suited to CCUS deployment?

TP: Large scale infrastructure companies like TC Energy have to lead the way. We have an incumbent position as operators of pipelines – the connective tissue for CCUS – and operators of subsurface storage assets – which gives us experience of managing geologic reservoirs. TC Energy owns and operate thermal cogeneration assets and have a stake in a large nuclear facility in Canada. Large companies are not always the fastest to move, but they are good at fitting the different pieces of the puzzle, the various motivations and the different risks, together. Permitting is a mess, because for Class VI permits, sometimes the EPA and sometimes the states have regulatory primacy, and the timelines for the different project development components do not always match. Many developers have failed, which creates more space in the market but highlights the challenges. It’s also important to understand where the demand for CCUS comes from, because that determines how the project gets financed and built. You need to understand a customer’s motivation - whether it’s simple decarbonisation or getting a premium for a carbon-free product. It’s hard to manage these relationships when you’re only responsible for one part of the value chain. For instance, it’s a bit of a “knife fight” on the US Gulf Coast right now, because everyone has a sequestration project in development, but they’re struggling to source CO2 offtake agreements, and economics have become more challenged since the IRA passed. Some customers just want a turnkey solution. They don’t necessarily care what happens to the CO2 as long as it’s sequestered no longer emitted, and prefer to get on with their core business.

DF: My pessimistic view is that the first projects are going to be borne on the shoulders of captive ratepayers with monopolistic utilities and will therefore be suboptimal. It will not be possible to work that way in ERCOT, where revenue visibility is one year ahead, not 30. It will be necessary to work with big infrastructure and E&P companies with big balance sheets. And the solution cannot be fragmented, even a company like NRG with a big thermal portfolio will need to work with third parties because we need to manage merchant risk as much as the banks.

JB: Large corporates will be in the best position to fund mega projects owing to their cost of capital and existing infrastructure. Private developers are nimble and will carve out their niche in the value chain in certain projects. Venture capital and government grants will initially fund new carbon capture technologies, followed by large corporate investments as the technology starts to mature.

BL: These challenges explain why we affiliated with Buckeye Partners, which has a large base of pipeline assets in regions with attractive storage opportunities. But the key will be getting recognition for the incremental value from decarbonisation, because carbon management is really waste management, and it has to be paid for. There’s a real purpose behind these projects – forestalling climate change – and the market will need to price in that service.

Proximo: What's our timeline to the first non-recourse deal, and what needs to happen first?

MG: Timing will be determined by identifying sufficient revenues to achieve financing.

LVA: We thought we might have 15 years to put together a combination of green hydrogen, small modular reactors and CCUS to fully decarbonise the US power grid, but we might need to start moving in the next five years to address the growing reliability risk. Without some additional “carrots and sticks” we could get another wave of natural gas-fired capacity additions which would raise concerns about meeting decarbonisation goals. CCUS is actually well positioned to respond to this near-term need and ensure the coming reliability crisis doesn’t go to waste.

BL: The first project financing gets done when we have the first long-term creditworthy offtake to support it. I think EPCs with appropriate guarantees are available. But we need an offtake that recognises the value of CCUS. If a project gets built on balance sheet, then that recognition has likely taken place internally at the company constructing the project.

TP: I think the market in general is waiting for some of these projects to actually take an FID [final investment decision]. We hear announcements every day - new agreements signed, FEED studies completed, government funding announcements. But no FID. A lot of people are “waiting and seeing”. Hopefully Project Tundra, TC Energy and Minnkota Power Cooperative’s project in North Dakota, will allow us to propagate new projects.